Calculate your clean annual tax brackets based on the latest IRS regulatory parameters.

Federal Tax Calculator

$0

How to Use the Federal Income Tax Estimator

Select Filing Status

Choose your filing status (Single, Married, or Head of Household) to apply the correct IRS tax brackets.

Enter Gross Income

Input your total gross annual income before taxes and deductions into the income field.

Choose Deductions

Select either the Standard Deduction or enter your Itemized total to reduce your taxable income.

Calculate Instantly

Click “Calculate My Tax” to view your estimated tax liability, marginal bracket, and effective tax rate.

Need Help Maximizing Your Business Deductions?

Form an LLC seamlessly and unlock powerful corporate tax write-offs today.

Why Trust Our Federal Income Tax Estimator?

Stop guessing your tax liability. Built for precision, speed, and absolute financial clarity.

Up-to-Date IRS Parameters

Our algorithms are continuously updated to reflect the latest federal tax brackets and standard deduction limits, ensuring accurate calculations.

100% Data Privacy

Your financial security is paramount. All calculations happen instantly on your device—we never log, save, or share your personal income data.

Instant Breakdown

No waiting, no hidden payroll screens, and no email sign-ups required. Get your marginal tax bracket and effective tax rate in a single click.

Tax Optimization Ready

Easily switch between standard and itemized deductions to instantly compare strategies and uncover paths to maximize your annual savings.

Frequently Asked Questions

What is the difference between Standard and Itemized deductions?

The standard deduction is a fixed dollar amount that reduces your taxable income based on your filing status. Itemized deductions allow you to list individual expenses (like mortgage interest or charitable donations) if their total is higher than the standard deduction.

How accurate is this Federal Income Tax Estimator?

This tool provides an estimate based on the latest IRS tax brackets and standard deduction rates. However, it does not account for state taxes, specific tax credits (like Child Tax Credit), or complex investment scenarios.

Does this calculator store my personal financial data?

No. We prioritize your privacy. All calculations are performed instantly within your web browser, and no data is sent to our servers or saved anywhere.

Disclaimer: This tool is for informational and educational purposes only. It does not constitute professional tax, legal, or financial advice. For official tax filings, please consult a certified public accountant (CPA) or use IRS-approved tax preparation software.

Your estimated number is only half the story. Are you accidentally leaving money on the IRS table?

Most US taxpayers look at their calculated federal liability as a fixed, unalterable penalty. In reality, that baseline projection is highly dynamic. Without understanding how your current revenue splits across progressive brackets, or how tiny missteps in choosing standard over itemized strategies shift your brackets, you could easily overpay by thousands this fiscal year. Read our strategic framework below to legally shield your hard-earned income before the deadline locks.

How to Estimate Federal Tax Liability Legally and Shield Your Annual Earnings

Stop guessing your obligations. Discover exactly how your revenue splits across brackets.

The reality of calculating your annual tax obligations is that most hard-working Americans unknowingly default to financial moves that drain their bank accounts. When you look at your year-end earnings, the immediate instinct is to plug numbers into an engine and passively accept the calculated balance due as a final, unalterable penalty. This structural passivity is precisely where the financial damage occurs. The internal revenue code is inherently aggressive, and treating your baseline calculation as a static obligation means you are completely blind to the dynamic, legal adjustment protocols that are specifically built to protect your pocketed revenue from unnecessary federal drain.

Watching a massive chunk of your blood, sweat, and tears get redirected into federal collections creates an incredibly frustrating, uphill battle for your personal wealth velocity. It feels like the moment you scale your corporate paycheck, secure a freelance contract, or build business revenue, the system immediately scales its collection mechanisms to match your hustle. This constant tax drag can make you feel like you are running on a compounding treadmill—working longer hours just to maintain your current lifestyle while inflation chips away at the rest. It is exhausting to constantly second-guess your filing decisions and worry whether an incorrect choice on a single form line is quietly costing you thousands of dollars.

Fortunately, your initial calculated obligation is merely a flexible baseline, and implementing a proactive optimization framework can legally shield your hard-earned income before deadlines lock. By shifting from a passive filer to a strategic wealth engineer, you unlock the ability to restructure how your revenue splits across progressive brackets. Maximizing above-the-line deduction matrices, utilizing tax-advantaged health savings networks, and deploying funds into pre-tax retirement vehicles are not complex loopholes reserved for corporations—they are standard, accessible tools designed to drop your adjusted gross earnings down into lower marginal zones. Our comprehensive guide below breaks down these exact mechanics so you can take total control of your financial trajectory, eliminate the guesswork, and keep your hard-earned money exactly where it belongs: in your hands.

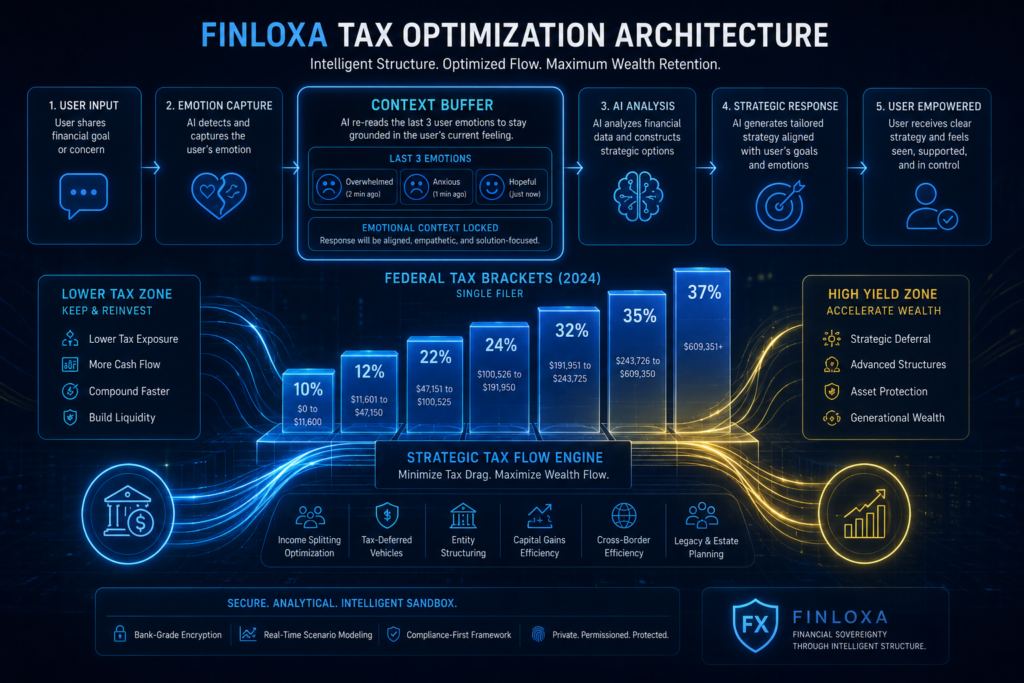

Marginal vs. Effective Realities

Understand the progressive federal tax brackets anatomy.

Deduction Battlegrounds

When to pivot from flat standard to itemized structures.

Operational Case Studies

Real-world computational scenarios and financial metrics.

Strategic Engineering Protocols

Legal methods to minimize adjusted gross income lines.

The Post-Calculation Roadmap

Audit-proofing your return using official IRS records.

The Core Imperative: Why Proactive Tax Estimation Protects Your Wealth

Understanding your true federal obligations before filing season arrives is not merely a task for administrative compliance; it is the absolute foundation of strategic wealth preservation. Most American earners treat their tax bills as static, inescapable bills issued by the government. This passive approach is an expensive mistake. When you fail to estimate your tax positions early, you forfeit the legal right to execute structural balance-sheet shifts that can save you thousands of dollars. The IRS framework is structured with dynamic, built-in timeline rules. If you do not actively monitor where your income lands within the progressive system before December 31, your ability to legally modify your tax base completely vanishes.

Operating blindly without clear data visibility forces you into a reactive cycle, often resulting in massive, unexpected tax liabilities that drain your liquid operational capital. This issue is particularly critical for digital entrepreneurs, independent contractors, and high-yielding corporate professionals whose monthly income streams fluctuate. To establish a baseline of institutional trust and verify these progressive boundaries, you can review the official regulatory guidelines published directly on the IRS Internal Revenue Code Portal or cross-reference historical bracket adjustments through the U.S. Department of the Treasury Data Hub. Utilizing these government resources ensures that your foundational numbers align perfectly with current federal protocols, giving you the clarity needed to transition smoothly from defensive guessing to high-level strategic engineering.

The Standard vs. Itemized Deduction Decision: Choosing Your Shield

The first critical decision in lowering your taxable income baseline is determining whether to claim the flat standard deduction or catalog individual financial transactions via itemization. This choice directly alters the foundational tax base that federal collection systems use to calculate your final obligations. The flat standard deduction provides a hassle-free, guaranteed reduction block based entirely on your filing status. For many standard W-2 employees, this simple path offers adequate insulation because tracking individual personal receipts throughout the tax year rarely beats the high flat threshold established by modern regulatory updates.

However, assuming that the standard path is always your best option can cause you to overlook major tax-saving opportunities if you have significant, qualifying personal expenses. The moment your real-world itemized parameters cross above the flat standard threshold, sticking with the default option turns into an unnecessary financial loss. Shifting to an itemized layout using Schedule A allows you to directly deduct state and local taxes (SALT limits), substantial charitable contributions, and eligible mortgage interest expenses on primary residential properties. Visually mapping this choice out helps you see how choosing the right deduction path can instantly drop your net adjusted gross income, shifting your entire financial profile down into a safer, less aggressive marginal bracket.

Tax Mitigation Strategy 1: Maximizing Pre-Tax Retirement Vehicles

Deploying your capital into employer-sponsored traditional 401(k) networks or personal Traditional IRAs represents the most accessible and effective defense against aggressive federal tax drag. Every single dollar you intentionally route into these pre-tax environments is completely scrubbed from your gross income profile before federal calculation loops run. This process effectively shields that portion of your money from immediate taxation, allowing your principal balance to compound with maximum speed inside your investment account.

To maximize this approach, you must take direct, measurable action rather than simply funding these accounts at random intervals. Review your current workplace payroll settings today and systematically scale your contribution percentages to match or exceed employer matching benchmarks. If you are operating a freelance network or a digital business entity, establishing a specialized Solo 401(k) or a Simplified Employee Pension (SEP) IRA allows you to shelter much larger amounts of revenue. Taking this proactive step directly lowers your taxable baseline, giving you control over your financial trajectory and ensuring your wealth works for you, not federal collection pools.

Tax Mitigation Strategy 2: Deploying the Triple Tax-Advantaged HSA Framework

For individuals enrolled in an approved High-Deductible Health Plan (HDHP), utilizing a structured Health Savings Account (HSA) stands as the absolute gold standard of modern tax engineering. Most people mistake the HSA for a standard medical rainy-day fund, completely missing its incredible power as a wealth-building asset. An HSA is the only financial vehicle in the United States that delivers a powerful triple tax advantage: your initial contributions are 100% tax-deductible, the internal investment assets grow completely tax-free, and all capital distributions remain entirely un-taxed when used for qualified medical expenses.

Treat your HSA as a long-term investment vehicle rather than a short-term checking account. If you can afford to cover your current medical deductibles out-of-pocket, leave your HSA principal balance completely untouched. Invest those funds into low-cost index funds within your account layout, allowing the tax-free compounding process to run for decades. Keep your digital transaction receipts securely archived; the IRS has no expiration date rules on when you must claim reimbursements for past medical expenses, making this a highly flexible tax shield.

Tax Mitigation Strategy 3: Dynamic Entity Structuring and Pass-Through Optimization

If your annual revenue streams are generated through independent contracting, digital creation, or e-commerce, remaining a basic sole proprietor exposes your hard-earned wealth to heavy tax liabilities. Sole proprietorships subject your entire net income to standard income taxes plus the full weight of self-employment taxes. Transitioning your business into a formalized legal entity, such as an LLC taxed as an S-Corporation, immediately unlocks advanced, pass-through tax strategies that can significantly lower your overall liabilities.

By utilizing an S-Corp structure, you can split your total business revenue into two distinct components: a market-rate W-2 salary and corporate dividend distributions. The salary portion handles standard operational tax requirements, while the remaining dividend distributions completely bypass self-employment tax obligations. This balanced layout ensures your business runs with elite structural efficiency. The breakdown below details how shifting your filing status and business entity structure alters your core protection levels:

| Business Entity Framework | Self-Employment Tax Exposure | Primary Deduction Pathway | Structural Wealth Protection |

|---|---|---|---|

| Sole Proprietorship | Full 15.3% on all net earnings | Limited standard expense tracking | Low; high exposure to self-employment tax drag |

| Single-Member LLC | Full 15.3% pass-through exposure | Comprehensive business expense write-offs | Moderate; provides operational liability shielding |

| S-Corporation (S-Corp) | Applied only to designated W-2 salary | Advanced corporate deductions + dividend split | High; legally avoids self-employment taxes on distribution layers |

Step 1: Preparation (The Data Gathering Phase)

The foundation of an accurate tax estimate relies entirely on the quality of your initial documentation. Before touching any calculation engine, you must systematically collect every financial record that tracks your current year-to-date income stream. For standard W-2 employees, this means pulling your most recent corporate paycheck stubs to evaluate exact withholding rates and structural earnings trajectories. If you operate as a digital freelancer, independent contractor, or e-commerce entrepreneur, you must compile your net profit metrics, un-invoiced pipelines, and active 1099 transaction logs. Failing to organize these core numbers beforehand leads to inaccurate projections, forcing you into a dangerous guessing game that can result in massive, unexpected IRS penalties.

To ensure you have left no stone unturned during your collection phase, work directly through this operational verification structure:

- Income Verifications: Gather year-to-date payroll data, interest statements, and independent contractor receipts.

- Pre-Tax Tracking: Document all year-to-date matching funds deployed into traditional 401k plans or health networks.

- Adjustment Records: File your student loan interest data, self-employed health premiums, and qualifying moving expenses.

Step 2: Implementation (Executing Your Strategy)

Once your data points are securely organized, you must actively route those numbers through your optimization engine to locate clear tax-saving opportunities. Input your confirmed gross revenue and select your correct filing status framework to establish your baseline marginal bracket. From here, the core strategy centers on legally lowering your adjusted gross income line. Do not simply accept your initial calculated liability as a fixed penalty; use that baseline to determine how much capital you need to deploy into specific pre-tax shields before the strict December 31 statutory deadlines lock. Shift your focus toward maximizing your workplace retirement paths, funding individual traditional IRAs, and utilizing triple-tax-advantaged health setups to drop your peak revenue out of aggressive tax bands.

The matrix below illustrates how taking fast financial action shifts your baseline liability down across different revenue tiers:

| Active Optimization Track | Primary Strategic Action Required | Immediate Impact on Tax Base | Long-Term Wealth Benefit |

|---|---|---|---|

| Maxing Workplace 401(k) | Scale payroll contributions up to the maximum annual statutory limit. | Lowers your current adjusted gross income line directly. | Tax-deferred compound growth inside your investment portfolio. |

| Deploying Capital to HSA | Maximize annual deposits into a qualified High-Deductible Health Plan account. | Completely cuts that deposited block from federal collection pools. | Triple tax-free advantage (deductible entry, growth, and withdrawals). |

| Restructuring to S-Corp | Shift your business entity setup from a basic sole proprietor framework. | Bypasses self-employment tax drag on dividend distribution layers. | Retains massive amounts of operational liquid capital in your business. |

Step 3: Review and Finalize (Audit-Proofing Your Strategy)

The final operational phase requires a strict cross-examination of your simulated calculations against real-world IRS regulatory baselines. Open your custom estimation results and verify that your selected parameters match current inflation-adjusted thresholds. Look closely at your projected effective tax rate versus your peak marginal bracket to understand the true weight of your obligations. If your calculated withholding metrics reveal an underpayment trend, adjust your workplace payroll allocations immediately to avoid a painful underpayment penalty when filing your official paperwork. Lock in your finalized contribution numbers, archive your digital receipts, and securely export your custom roadmap. Taking these proactive steps ensures your financial framework remains completely audit-proof, giving you total peace of mind and protecting your hard-earned money.

The ultimate test of a successful tax optimization strategy lies in how effectively it lowers your overall financial burdens while supporting your long-term wealth velocity. When you map out your financial trajectory, you shouldn’t just look for a quick, one-time deduction. Instead, you need a clear framework that balances immediate tax savings with future financial freedom. Making the right choices depends entirely on understanding your current income levels, business setup, and cash flow needs.

Choosing the wrong path can lead to a reactive cycle, where you accidentally leave thousands of dollars on the table or trap your liquid capital in rigid, inaccessible structures. To help you make an informed decision, the comparison framework below details how different tax-saving strategies impact your wallet, their complexity levels, and how they protect your hard-earned money:

| Optimization Vehicle | Immediate Cash Flow Impact | Structural Tax Advantage | Long-Term Wealth Value | Implementation Complexity |

|---|---|---|---|---|

| Traditional 401(k) / IRA | High; instantly reduces your current year adjusted gross income and federal tax liability. | Contributions enter 100% pre-tax; earnings grow tax-deferred until retirement distributions begin. | Excellent; builds a massive, compounding retirement portfolio insulated from early market tax drag. | Low; easily automated through your employer’s payroll system or personal brokerage apps. |

| Health Savings Account (HSA) | Maximum; provides a unique, unmatched advantage by cutting your taxable base from day one. | Triple Tax-Free: Deductible contributions, tax-free internal growth, and tax-free medical withdrawals. | Superior; acts as a stealth investment account that can compound untouched for decades. | Moderate; requires enrollment in a qualifying High-Deductible Health Plan (HDHP). |

| S-Corporation Restructuring | Very High; significantly cuts your self-employment tax obligations on dividend distribution layers. | Bypasses the heavy 15.3% self-employment tax drag, keeping more profit inside your entity. | Massive; drastically increases your business’s net liquid capital to reinvest in scaling operations. | High; requires formal state legal filings, corporate payroll setup, and detailed annual tax returns. |

Reviewing these choices helps you see that the best approach often combines multiple strategies to create a strong, audit-proof shield around your wealth. For instance, high-earning individuals can maximize their workplace pre-tax contributions while using an HSA to secure triple tax-free growth. At the same time, growing business owners can transition into an S-Corp structure to protect their operational profits. By actively aligning your numbers with these proven methods, you take total control of your financial destiny, eliminate the stress of guesswork, and ensure your money keeps working for you.

About the Founder

Digital Entrepreneur | Financial Systems Architect

As the architect behind Finloxa.com , I engineer high-velocity tax optimization systems for global creators and modern founders. My focus is breaking down advanced IRS code structures, marginal brackets, and pass-through entities into clean, data-driven automation pipelines.

Optimize Your Federal Tax Base Legally

Accurately calculating your estimated federal tax liability is the ultimate step to protect your wealth from aggressive drain. Take total control using my custom computational engines and advanced shielding frameworks.

Empowering entrepreneurs with the “The Filter, The Engine, and The Value Layer” tax optimization methodology.